The Bank of England studies inflationary trends in the economy. This involves looking at a range of economic variables such as:

From these statistics, the Bank of England decides whether inflation is likely to rise or fall.

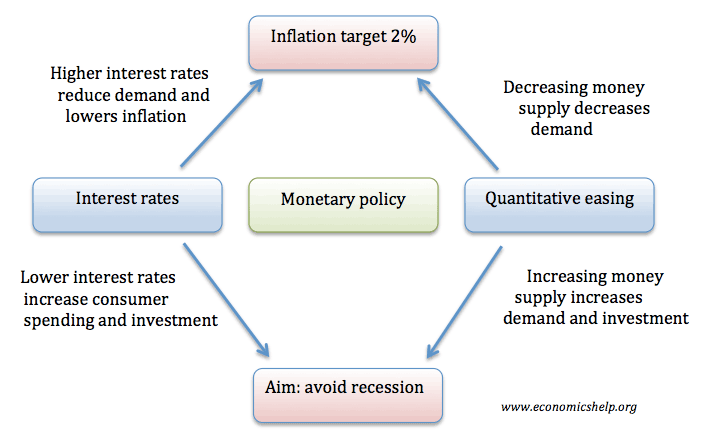

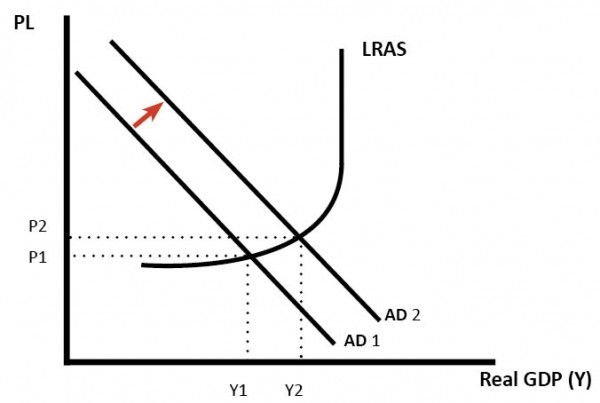

During the credit crunch of 2008-09, the Bank of England also used Quantitative Easing as a part of monetary policy. This involves creating money electronically to buy assets (such as government bonds from banks). It is hoped by buying illiquid assets there will be an increase in the money supply and avoid deflationary pressures.

If the Bank of England anticipates inflation falling below the government’s target of 2% and economic growth is sluggish, or the economy is facing a recession. They are likely to cut interest rates.

Lower interest rates, in theory, should stimulate economic activity. This is because lower interest rates reduce borrowing costs. This increases the disposable income of consumers with mortgage interest payments and should encourage spending.

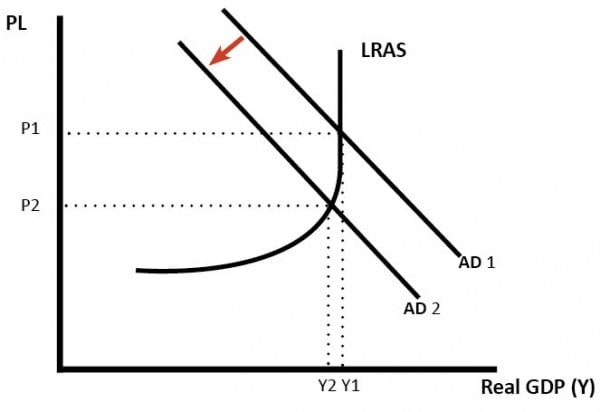

If the Bank feels the economy is growing too quickly and inflation is expected to exceed the government’s target, then they are likely to increase interest rates to reduce the rate of economic growth and reduce inflationary pressures.

In this case, a rise in interest rates causes a fall in consumer spending and investment leading to lower inflation.

Since the financial crisis of 2009, economic growth has been sluggish and inflationary pressures low. Therefore, the Bank of England has kept interest rates at record low levels.

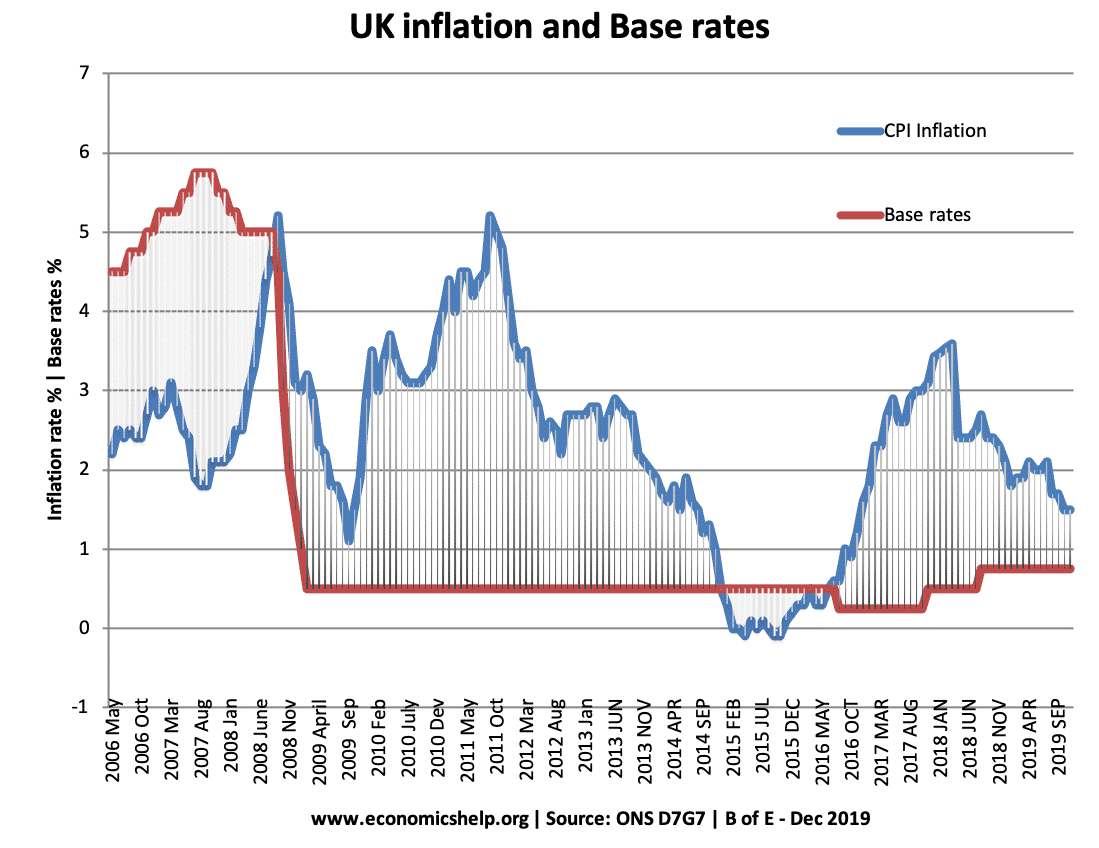

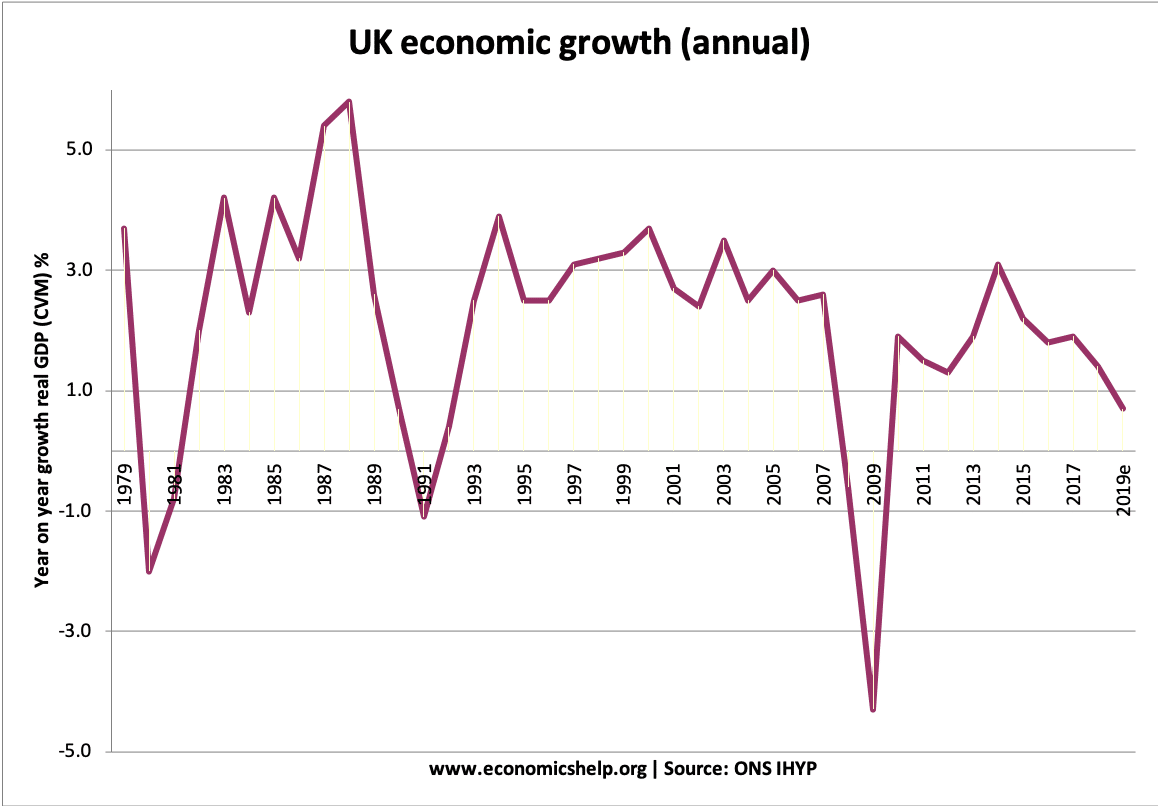

In 2008/09, the economy went into deep recession. This led the Bank of England to cut interest rates from 5% to 0.5%.

1997-2007

In the period 1997-2007, monetary policy effectively kept economic growth and inflation stable. This was because cost-push inflation was low and the independent Bank of England was successful in preventing growth exceeding the long-run trend rate.

However, in the great moderation, despite low inflation, there were imbalances in the economy – such as rising house prices and boom in credit. This shows the limit of monetary policy in preventing a credit bubble.

Between 2007 and 2011, monetary policy became much more difficult. This was because of:

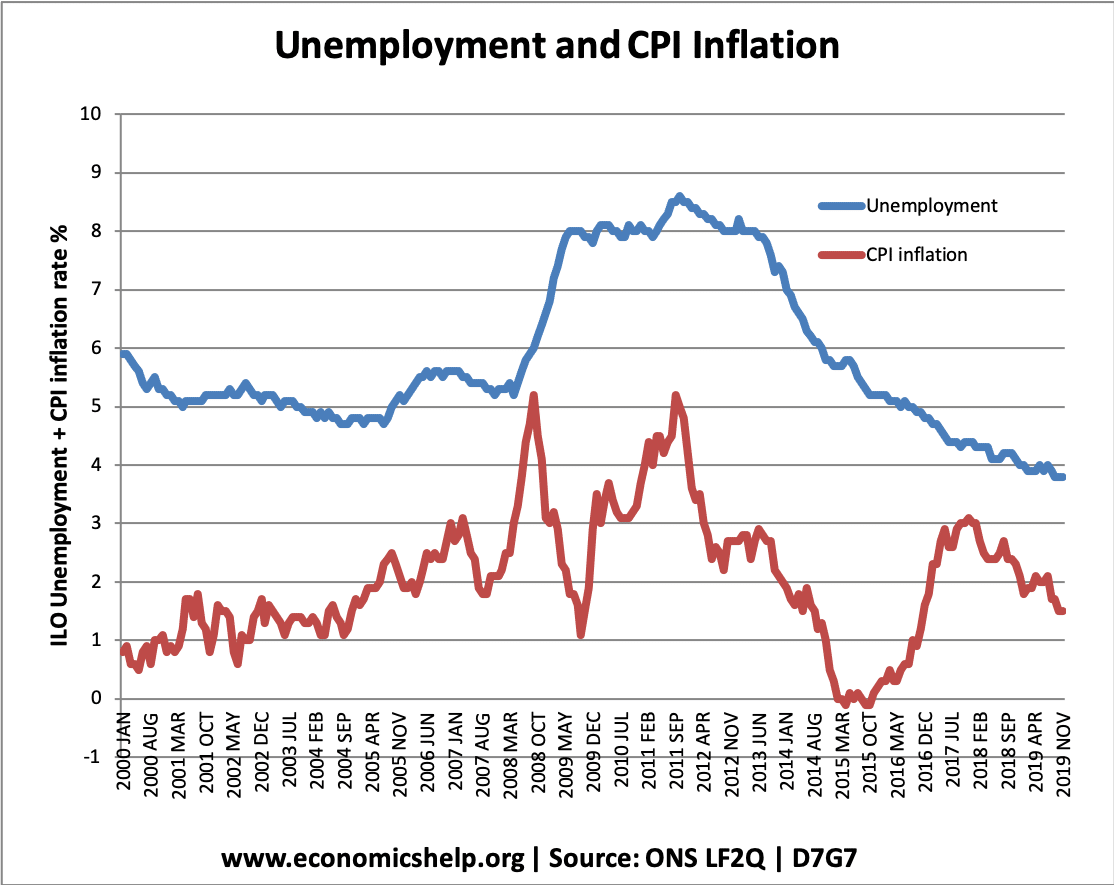

Cost-push inflation and recession. In 2008 and 2011, the UK experienced a rise in CPI inflation to over 5%. (see: cost push inflation) Yet, at the same time, economic growth was very low or negative. This present the Bank of England with a difficulty. On the one hand, inflation is above their target so they should consider raising interest rates. However, with a depressed economy, the economy needs the opposite.

Liquidity Trap. In 2008, the economy was in a liquidity trap. Cutting interest rates to zero, failed to boost spending and economic growth. Therefore, the Bank of England were forced to pursue quantitative easing.

Some limitations of monetary policy include:

See also: