Demand for housing was incredibly strong through 2020 and 2021 as record-low mortgage rates and high personal savings helped create a homebuying frenzy. But times have changed quickly. While the housing market isn’t crashing, rising rates and persistently high home prices have caused mortgage demand to significantly diminish from where it stood at the beginning of 2022.

Nonetheless, Americans owe $12.14 trillion on their mortgages, and mortgage debt accounts for 70.2% of consumer debt in the U.S. Even with interest rates hovering above 7.00%, mortgage demand hasn’t disappeared, and Americans across the country are trying to navigate today’s challenging housing market. Because of this, understanding how Americans deal with their mortgages is fundamental to comprehending the state of American finances.

With that in mind, LendingTree analyzed various data sources to create a mortgage statistics overview. Read on to learn more about how much mortgage debt Americans have — and how they use and manage that debt.

The massive increase in outstanding mortgage debt has been driven by two things: more people with active mortgages and mortgages that are (generally) larger.

Record-low mortgage interest rates allowed many buyers to increase their purchase prices — or take advantage of cash-out refinances — while maintaining similar monthly payments to what was available in the recent past with smaller loan sizes.

Outstanding mortgages

| Mortgage accounts* (millions) | Mortgage balances ($ trillions) | Average mortgage size per account | |

|---|---|---|---|

| Q4 2012 | 83.23 | $8.03 | $96,516 |

| Q4 2013 | 81.60 | $8.05 | $98,640 |

| Q4 2014 | 81.43 | $8.17 | $100,332 |

| Q4 2015 | 80.61 | $8.25 | $102,332 |

| Q4 2016 | 79.90 | $8.48 | $106,133 |

| Q4 2017 | 79.99 | $8.88 | $111,039 |

| Q4 2018 | 79.35 | $9.12 | $114,984 |

| Q4 2019 | 80.94 | $9.56 | $118,075 |

| Q4 2020 | 80.60 | $10.04 | $124,603 |

| Q4 2021 | 80.96 | $10.93 | $135,005 |

| Q4 2022 | 83.42 | $11.92 | $142,927 |

| Q3 2023 | 83.96 | $12.14 | $144,593 |

Source: LendingTree analysis of Federal Reserve Bank of New York data. Notes: *People with joint accounts are counted twice if a mortgage account appears on their credit report. 2023 data is through the third quarter.

Outstanding HELOCs

| HELOC accounts* (millions) | HELOC balances ($ trillions) | Average HELOC size per account | |

|---|---|---|---|

| Q4 2012 | 18.66 | $0.56 | $30,171 |

| Q4 2013 | 17.71 | $0.53 | $29,870 |

| Q4 2014 | 17.26 | $0.51 | $29,548 |

| Q4 2015 | 16.68 | $0.49 | $29,197 |

| Q4 2016 | 16.26 | $0.47 | $29,090 |

| Q4 2017 | 15.68 | $0.44 | $28,316 |

| Q4 2018 | 15.41 | $0.41 | $26,736 |

| Q4 2019 | 14.99 | $0.39 | $26,017 |

| Q4 2020 | 13.75 | $0.35 | $25,382 |

| Q4 2021 | 12.75 | $0.32 | $24,941 |

| Q4 2022 | 13.12 | $0.34 | $25,610 |

| Q3 2023 | 13.07 | $0.35 | $26,702 |

Source: LendingTree analysis of Federal Reserve Bank of New York data. Notes: *People with joint accounts are counted twice if a HELOC account appears on their credit report. 2023 data is through the third quarter.

Mortgage interest rates for a 30-year, fixed loan peaked at 18.63% in 1981. The weekly average for that year was 16.64%. In fact, rates didn’t drop below 10.00% between November 1978 and April 1986.

Over the past 50 years, rates dropped below 5% for the first time in 2009 after the Federal Reserve aggressively lowered target rates to combat the Great Recession of 2007 to 2009. Rates dipped below 4% for the first time in late 2011 and below 3% for the first time in 2020.

Average mortgage rates reached their lowest level (2.65%) during the first week of 2021. The lowest weekly rate in the 30 years between 1972 and 2001 — 6.45% — occurred in November 2001. But weekly average mortgage rates were back above 7.00% in August 2023 for the first time since November 2022. The 7.79% average for the week of Oct. 26, 2023, was the highest in more than 20 years.

Here’s a look at historic mortgage rates dating to 1972:

Historic interest rates for 30-year conventional mortgages

| Year | Annual weekly average | Annual high | Annual low |

|---|---|---|---|

| 1972 | 7.38% | 7.46% | 7.23% |

| 1973 | 8.04% | 8.85% | 7.43% |

| 1974 | 9.19% | 10.03% | 8.40% |

| 1975 | 9.05% | 9.60% | 8.80% |

| 1976 | 8.87% | 9.10% | 8.70% |

| 1977 | 8.85% | 9.00% | 8.65% |

| 1978 | 9.64% | 10.38% | 8.98% |

| 1979 | 11.20% | 12.90% | 10.38% |

| 1980 | 13.74% | 16.35% | 12.18% |

| 1981 | 16.64% | 18.63% | 14.80% |

| 1982 | 16.04% | 17.66% | 13.57% |

| 1983 | 13.24% | 13.89% | 12.55% |

| 1984 | 13.88% | 14.68% | 13.14% |

| 1985 | 12.43% | 13.29% | 11.09% |

| 1986 | 10.19% | 10.99% | 9.29% |

| 1987 | 10.21% | 11.58% | 9.03% |

| 1988 | 10.34% | 10.77% | 9.84% |

| 1989 | 10.32% | 11.22% | 9.68% |

| 1990 | 10.13% | 10.67% | 9.56% |

| 1991 | 9.25% | 9.75% | 8.35% |

| 1992 | 8.39% | 9.03% | 7.84% |

| 1993 | 7.31% | 8.07% | 6.74% |

| 1994 | 8.38% | 9.25% | 6.97% |

| 1995 | 7.93% | 9.22% | 7.11% |

| 1996 | 7.81% | 8.42% | 6.94% |

| 1997 | 7.60% | 8.18% | 6.99% |

| 1998 | 6.94% | 7.22% | 6.49% |

| 1999 | 7.44% | 8.15% | 6.74% |

| 2000 | 8.05% | 8.64% | 7.13% |

| 2001 | 6.97% | 7.24% | 6.45% |

| 2002 | 6.54% | 7.18% | 5.93% |

| 2003 | 5.83% | 6.44% | 5.21% |

| 2004 | 5.84% | 6.34% | 5.38% |

| 2005 | 5.87% | 6.37% | 5.53% |

| 2006 | 6.41% | 6.80% | 6.10% |

| 2007 | 6.34% | 6.74% | 5.96% |

| 2008 | 6.03% | 6.63% | 5.10% |

| 2009 | 5.04% | 5.59% | 4.71% |

| 2010 | 4.69% | 5.21% | 4.17% |

| 2011 | 4.45% | 5.05% | 3.91% |

| 2012 | 3.66% | 4.08% | 3.31% |

| 2013 | 3.98% | 4.58% | 3.34% |

| 2014 | 4.17% | 4.53% | 3.80% |

| 2015 | 3.85% | 4.09% | 3.59% |

| 2016 | 3.65% | 4.32% | 3.41% |

| 2017 | 3.99% | 4.30% | 3.78% |

| 2018 | 4.54% | 4.94% | 3.95% |

| 2019 | 3.94% | 4.51% | 3.49% |

| 2020 | 3.11% | 3.72% | 2.66% |

| 2021 | 2.96% | 3.18% | 2.65% |

| 2022 | 5.34% | 7.08% | 3.22% |

| 2023 | 6.79% | 7.79% | 6.09% |

Source: LendingTree analysis of Federal Reserve of St. Louis data. Note: 2023 data is as of the week of Nov. 16.

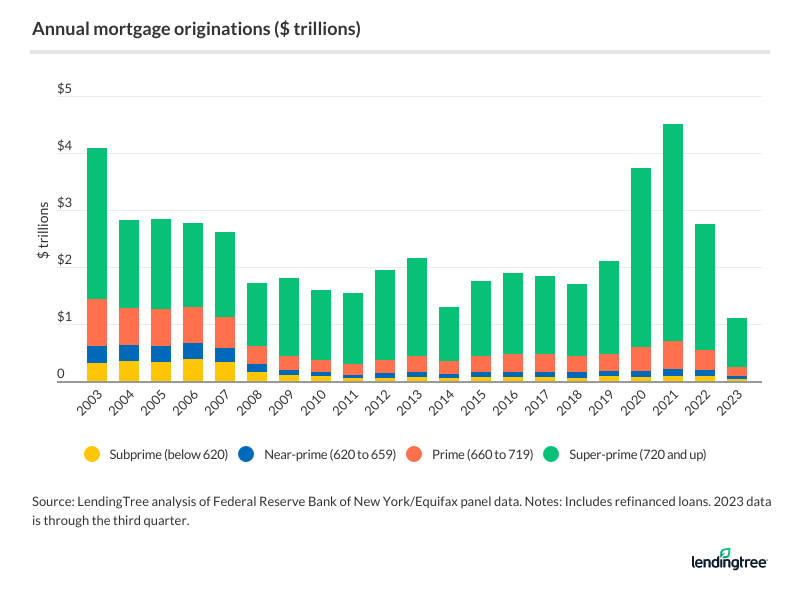

Mortgage originations dropped off dramatically as rates rose from their 2021 historic lows. In fact, mortgage originations totaled $2.75 trillion in 2022, compared with $4.51 trillion in 2021. Originations in 2023 are on pace to cut 2022’s number in half — $1.1 trillion in the first three quarters of this year, compared with $2.2 trillion the prior year.

At $4.51 trillion, 2021 saw the largest annual origination volume of the past 20 years. Historically low rates that year meant that borrowers could take out bigger loans for similar monthly payments, and it also drew many people to refinance their existing mortgages.

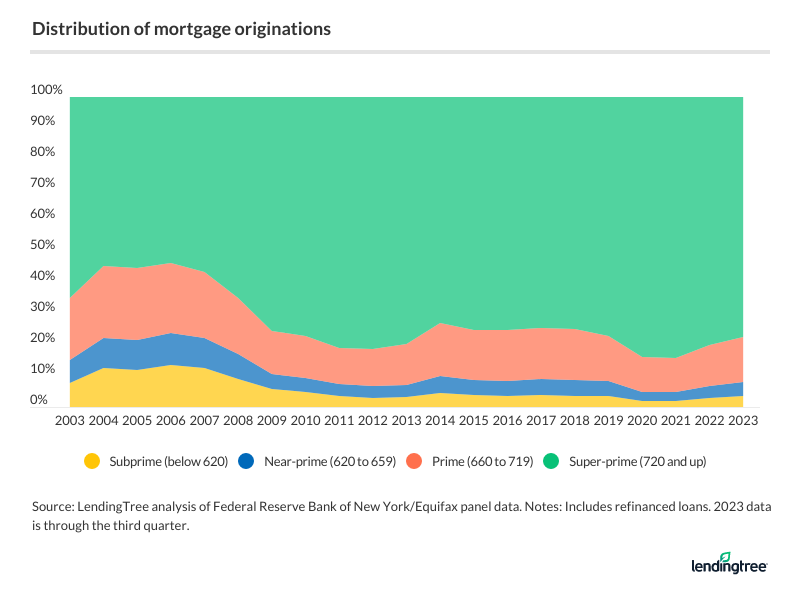

Origination volume was also elevated in the years leading up to the subprime mortgage financial crisis of 2007 to 2010, with subprime borrowers with credit scores below 620 taking up an unusually large share of the new debt. Subprime borrowing as a share of origination volume peaked in 2006 at 13.6%, while super-prime borrowers with scores of at least 720 held their smallest share that year (53.5%). In 2020 and 2021, subprime borrowers only comprised around 2% of the volume, while super-prime borrowers comprised around 84%.

The amount borrowed for home purchases varies greatly by location — and local home purchase prices.

The average amount borrowed through our platform to purchase a home — which excludes down payments and closing fees — ranged from $464,994 in Hawaii to $150,245 in West Virginia in the 12 months ending in October 2023.

How much people borrowed for home purchases via the LendingTree platform in the 12 months ending on Oct. 31, 2023

| State | Average mortgage size | Size rank |

|---|---|---|

| Overall | $224,398 | – |

| Alabama | $197,289 | 35 |

| Alaska | $301,524 | 5 |

| Arizona | $237,587 | 19 |

| Arkansas | $183,259 | 39 |

| California | $287,865 | 9 |

| Colorado | $299,619 | 6 |

| Connecticut | $226,073 | 24 |

| Delaware | $246,848 | 17 |

| District of Columbia | $355,986 | 2 |

| Florida | $234,919 | 21 |

| Georgia | $222,409 | 26 |

| Hawaii | $464,994 | 1 |

| Idaho | $250,907 | 16 |

| Illinois | $190,790 | 36 |

| Indiana | $161,580 | 48 |

| Iowa | $153,405 | 50 |

| Kansas | $177,418 | 41 |

| Kentucky | $180,151 | 40 |

| Louisiana | $167,427 | 45 |

| Maine | $201,270 | 33 |

| Maryland | $255,009 | 15 |

| Massachusetts | $309,490 | 3 |

| Michigan | $160,707 | 49 |

| Minnesota | $223,078 | 25 |

| Mississippi | $166,939 | 46 |

| Missouri | $183,905 | 38 |

| Montana | $244,883 | 18 |

| Nebraska | $199,875 | 34 |

| Nevada | $278,693 | 11 |

| New Hampshire | $277,867 | 12 |

| New Jersey | $262,107 | 13 |

| New Mexico | $218,578 | 30 |

| New York | $229,268 | 23 |

| North Carolina | $234,641 | 22 |

| North Dakota | $174,820 | 44 |

| Ohio | $165,297 | 47 |

| Oklahoma | $177,088 | 42 |

| Oregon | $280,468 | 10 |

| Pennsylvania | $175,427 | 43 |

| Rhode Island | $288,874 | 8 |

| South Carolina | $218,692 | 29 |

| South Dakota | $220,202 | 27 |

| Tennessee | $218,175 | 31 |

| Texas | $235,867 | 20 |

| Utah | $295,704 | 7 |

| Vermont | $207,129 | 32 |

| Virginia | $258,027 | 14 |

| Washington | $308,031 | 4 |

| West Virginia | $150,245 | 51 |

| Wisconsin | $187,202 | 37 |

| Wyoming | $219,171 | 28 |

Source: Anonymized LendingTree data.

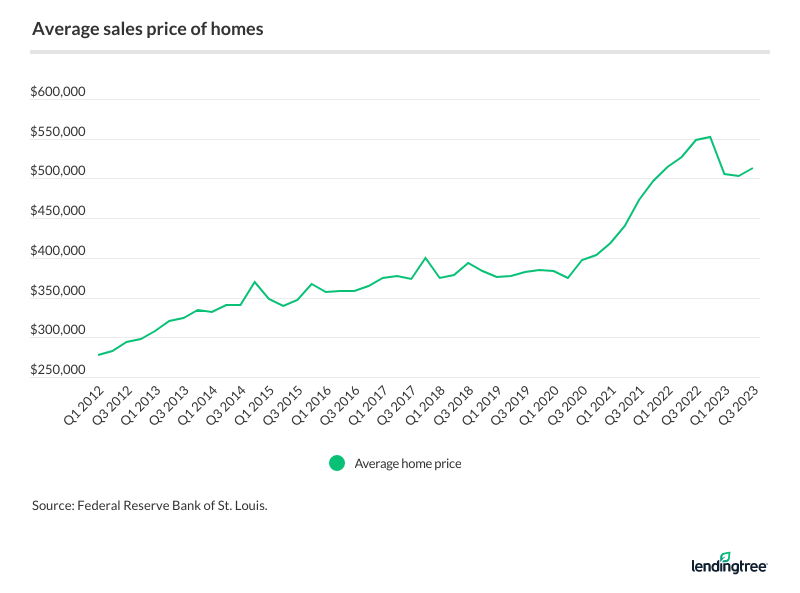

Meanwhile, the average purchase price for a home in the U.S. — including down payments — was dramatically higher than the $224,398 average mortgage size on our platform between November 2022 and October 2023. The average home price reached its historic high nationally in the fourth quarter of 2022, at $552,600, but it dropped to $513,400 in the third quarter of 2023.

Driven in part by lower mortgage rates, home prices rose dramatically after the start of the pandemic, when the national average home purchase price was $374,500. There was an increase of $178,100, or 47.6%, in the 2.5 years before the peak in the fourth quarter of 2022. Even with the decrease in prices, the average price was $138,900 higher in the third quarter of 2023, or 37.1% higher, than at the start of the pandemic.

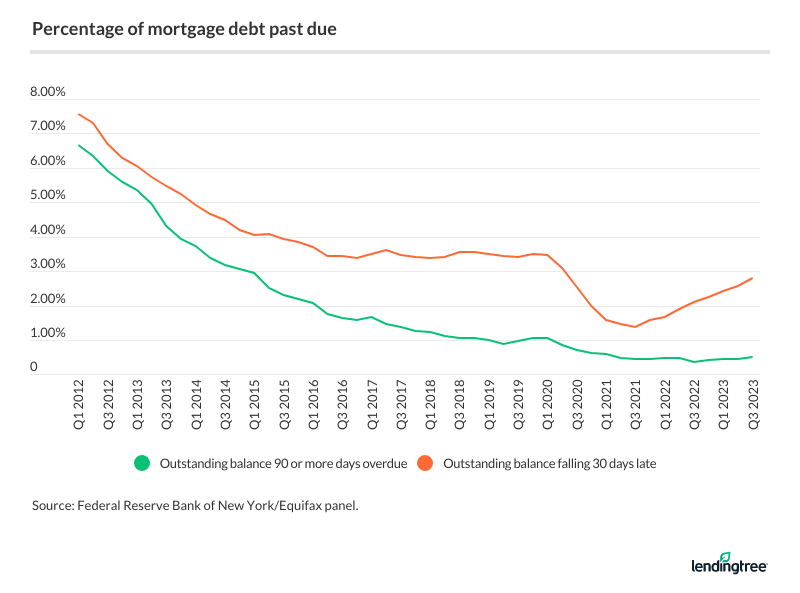

The percentage of mortgage debt that’s seriously delinquent — meaning 90 days or more past due — is near a historic low. However, it’s important to remember that this represents the percentage of outstanding debt, not the number of individual accounts.

According to the Federal Reserve Bank of New York, 0.5% of mortgage debt was at least 90 days late in September 2023. Based on the rate of seriously delinquent loans in August 2023 (the latest available data from CoreLogic), this roughly translated to 1.2% of individual loans.

As discussed, 2021 saw a huge surge in the total volume of dollars originated as mortgage debt, and a historically high proportion of that went to super-prime borrowers, which should minimize the amount of debt that becomes delinquent or goes into foreclosure.

However, there’s a point of concern for the future. The amount of mortgage debt that became 30 days overdue began to rise at the end of 2021 following drastic drop-offs during the pandemic. Most of these borrowers will catch up shortly, but every delinquency begins with one missed payment.

Number of new foreclosures

| Year | Foreclosures |

|---|---|

| 2012 | 451,340 |

| 2013 | 708,140 |

| 2014 | 495,620 |

| 2015 | 404,180 |

| 2016 | 339,200 |

| 2017 | 314,220 |

| 2018 | 284,360 |

| 2019 | 277,560 |

| 2020 | 129,000 |

| 2021 | 38,040 |

| 2022 | 122,140 |

| 2023 | 110,600 |

Source: Federal Reserve Bank of New York/Equifax panel. Note: 2023 data is through the third quarter.